Mat Credit Entitlement Entry

Image Result For Pch Official Entry Forms Publisher Clearing House Pch Sweepstakes Pch

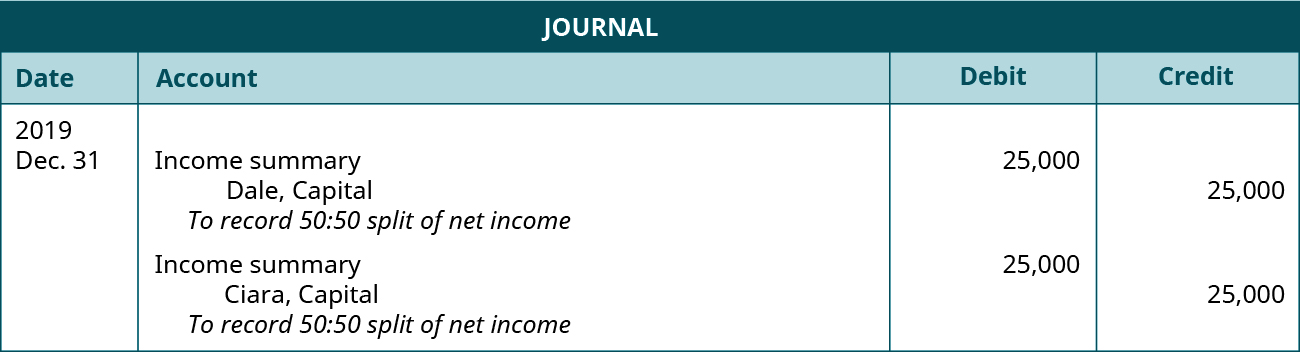

Compute And Allocate Partners Share Of Income And Loss Principles Of Accounting Volume 1 Financial Accounting

Income Tax Provision Entry In Tally Provision For Income Tax Entry In Tally Part 1 Youtube

Access Acaps

Coronavirus Information

Pin By Elaine Linderman On Check S Winning Numbers Publisher Clearing House Pch Sweepstakes

The mat credit may however be shown separately as mat credit entitlement account.

Mat credit entitlement entry.

Sap Absence Quota Generation Rules Tutorial Free Sap Hr Training

Http Www Rmbstrusteesettlement Com Docs Doc 20477 Pdf

Guide To Minimum Alternate Tax For Ind As Compliant Companies

Curriculum Guide Simplebooklet Com

Form I 864 Affidavit Of Support Help Center Chodorow Law Offices

Significant Accounting Policies Mindtree

Pay Statement Explained Opa

How Do We Account For The Mat And Mat Credit Quora

Https Www2 Deloitte Com Content Dam Deloitte In Documents Tax In Tax Minimum Alternate Companies Noexp Pdf

Https Becomeaprovider Amerihealthcaritas Com Pdf New Hampshire Provider Manual Pdf

Sec Filing Just Energy Group Inc

As 22 What Is Mat Credit Youtube

Covid 19 Human Resources University Of Connecticut

Http Castro Tea State Tx Us Charter Apps Content Downloads Nocdn 22 30 Pdf

Http Castro Tea State Tx Us Charter Apps Content Downloads Nocdn 21 22 Pdf

Retiring Partner Final Payment To Retiring Partner Journal Entries

Involuntary Psychiatric Hospitalization Appeals Case Preparation

Http Catalog Sunyocc Edu Mime Media 4 577 2011 2012 College Catalog Pdf

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcrknxbiewgugjjpwdn8qb0xhagyqgje70vfwzddgzikwjjxaw7s Usqp Cau

Https Help Sap Com Doc C3542f9df2424288bed9f041dd58c705 2 0 En Us Sap Pra 200 Application Help Pdf

Mat Credit An Overview Of Its Rationale And Impact

Http Library Com Edu Comhistory Catalogs 20072008catalog Pdf

Https Www Gpo Gov Fdsys Pkg Fr 1952 05 16 Pdf Fr 1952 05 16 Pdf

Https Sac Edu Catalogandschedule Documents 2020 2021 Sac Catalog 2020 2021 Pdf

Source : pinterest.com